Are you worried that replacing something valuable might make your insurance premium go up? You’re not alone.

Many people ask, “Will my insurance premium increase after replacement? ” It’s a common concern because no one wants unexpected costs. Understanding how replacement affects your insurance can save you money and stress. Keep reading to discover what really happens to your premium and how you can protect your wallet.

)

Credit: insurify.com

Factors Influencing Premium Changes

Insurance premiums can change after a vehicle replacement. Several factors influence whether the premium will rise or stay the same. Understanding these factors helps you prepare for any cost changes.

Impact Of Vehicle Replacement

The type of new vehicle affects your premium. A more expensive car usually costs more to insure. Safety features and repair costs also matter. Replacing an old car with a newer model can lower or raise your premium. The vehicle’s risk level plays a key role.

Role Of Claim History

Your past claims impact premium changes. More claims may lead to higher premiums. Insurance companies see frequent claims as higher risk. A clean claim history often helps keep premiums stable. After replacement, your claim record still matters.

Effect Of Vehicle Age And Model

Older vehicles often have lower premiums. Newer models might cost more to insure. Some models are cheaper to repair, lowering costs. Classic or rare cars can have different rates. The vehicle’s age and model influence premium adjustments.

Credit: centennialroofing.com

How Insurance Companies Calculate Premiums

Insurance companies use several factors to decide your premium. They study risks and the value of what you want to protect. This helps set a fair price for your policy. Understanding this process shows why premiums might change after replacement.

Risk Assessment Methods

Insurance firms check many risks before setting premiums. They look at your location, age, and claims history. They also consider the likelihood of damage or loss. The higher the risk, the higher the premium might be.

Use Of Replacement Value In Pricing

Replacement value is the cost to fix or replace your item. Insurers calculate premiums based on this value. If you replace something with a more expensive item, premiums may rise. This is because the cost to insure the new item is higher.

Influence Of Policy Type

Different policies cover different risks and amounts. A full coverage policy costs more than a basic one. The type of policy you choose affects your premium. Changing your policy after replacement can change your premium too.

When Premiums Typically Increase

Insurance premiums can change for several reasons. Knowing when these changes happen helps you prepare better. Premiums usually increase due to certain common situations. These relate to your claims, coverage, or vehicle changes. Understanding these can help you manage your insurance costs.

After Major Claims Or Replacements

Filing a big claim often leads to higher premiums. Insurers see major claims as higher risk. Replacing parts or the entire vehicle after damage can signal future costs. This makes the insurer raise your premium. Small claims might not affect your premium much. Large claims or frequent claims usually cause increases.

Changes In Coverage Limits

Increasing your coverage limits raises your premium. Higher limits mean the insurer covers more in damage or loss. This added protection costs more. Lowering limits can reduce premiums. But it also lowers your protection. Adjusting your coverage needs affects your premium directly.

Adjustments Due To Vehicle Upgrades

Upgrading your vehicle can increase your insurance premium. New features or higher value make repairs costlier. Luxury or performance upgrades often lead to higher premiums. Insurers factor in the replacement cost and repair difficulty. These adjustments help cover the extra risk they take.

Strategies To Avoid Premium Hikes

Insurance premiums can rise after a replacement. This increase depends on several factors. Knowing ways to keep premiums steady helps save money. These strategies work well for many policyholders.

Smart choices and good habits prevent sudden premium hikes. Careful planning can keep your insurance costs manageable. Focus on these simple steps to avoid paying more.

Choosing The Right Deductible

Selecting a higher deductible lowers your premium. You pay more out-of-pocket during a claim. This choice suits those who want lower monthly costs. Balance your deductible with your ability to pay if needed.

Maintaining A Clean Claim Record

A claim-free record helps keep premiums low. Filing many claims signals risk to insurers. Avoid small claims to protect your rates. Drive safely and maintain your property well.

Comparing Insurance Providers

Different insurers offer various rates for similar coverage. Shop around to find the best premium. Switching providers can reduce your insurance costs. Review policies annually to stay updated on offers.

Alternatives To Manage Replacement Costs

Replacement costs can add up quickly and affect your insurance premiums. Managing these costs helps keep your expenses low. There are several alternatives to consider that can ease the financial burden.

These options help protect your wallet and may prevent big jumps in your premium.

Gap Insurance Options

Gap insurance covers the difference between your car’s value and the amount you owe. It helps if your car is totaled or stolen. This coverage reduces out-of-pocket costs for replacements. Many drivers find it useful to avoid large bills after accidents.

Using Oem Vs. Aftermarket Parts

OEM parts come from the car manufacturer and usually cost more. Aftermarket parts are cheaper and still work well. Choosing aftermarket parts can lower repair and replacement costs. Insurers may prefer aftermarket parts to keep claims affordable.

Negotiating With Insurers

Talk to your insurer about your replacement options. Ask if they offer discounts or flexible plans. Negotiating can lead to better rates or lower premiums. Being clear about your needs helps insurers find the best solution.

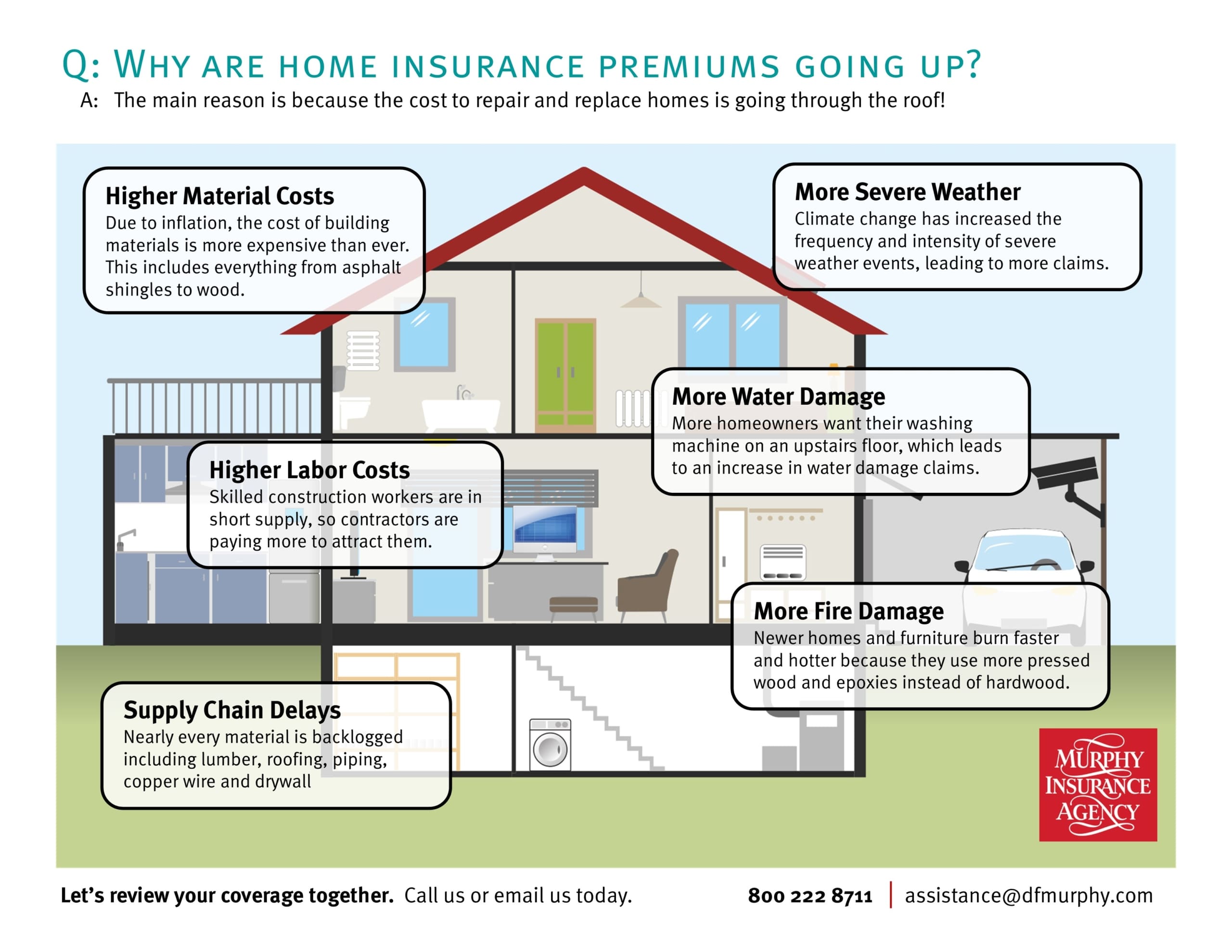

Credit: www.dfmurphy.com

Frequently Asked Questions

Will My Insurance Premium Increase After Replacement?

Your insurance premium might increase after replacement if the new item is more valuable. Insurers assess risk based on the replacement cost. Higher value or upgraded items usually lead to higher premiums. Always check with your insurer before replacing to understand potential premium changes.

How Does Replacement Affect Insurance Premium Calculation?

Replacement affects premium as insurers reassess the item’s current value. If the replacement costs more, premiums often rise. Some policies consider depreciation, so a new item may change coverage terms. Understanding your policy’s terms helps predict how replacement impacts your premium.

Can I Avoid Premium Hikes After Item Replacement?

To avoid premium hikes, inform your insurer about replacements promptly. Choose replacements with similar value and features to minimize changes. Some insurers offer flexible plans that adjust coverage without immediate premium increases. Always compare options before replacing insured items.

Does Insurance Always Cover The Full Replacement Cost?

Not always. Coverage depends on your policy type and limits. Some policies cover actual cash value, deducting depreciation. Replacement cost coverage pays full replacement price but may cost more. Review your policy details to know your coverage scope after replacement.

Conclusion

Replacing an item can change your insurance premium. Sometimes, the cost goes up because the new item is more expensive. Other times, it stays the same if the replacement matches the old one. Always tell your insurer about any replacement.

This helps keep your coverage accurate and avoid surprises. Understanding these factors saves money and stress. Keep your policy updated for the best protection. Simple steps make a big difference in managing costs.

Leave a Reply